RWA Tokenization: A Complete Guide to Tokenomics Design for Real-World Assets

RWA tokenization converts real-world asset ownership into on-chain tokens. Learn how to design tokenomics for tokenized real estate, credit, and infrastructure.

RWA tokenization is the process of representing ownership or economic rights in a real-world asset as a cryptographic token on a blockchain. Real estate, private credit, infrastructure, commodities, and revenue-generating businesses are all candidates. The token holds the legal claim or economic entitlement; the blockchain handles settlement, yield distribution, and transfer enforcement.

Most guides stop at that definition. This one covers what comes after it: how to design the tokenomics. Revenue mechanics, compliance structure, supply architecture, and liquidity strategy, the four decisions that determine whether a tokenized asset succeeds or collapses.

Getting the definition right is the starting point. Getting the design right is where most projects fail.

Learn about our tokenomics consulting approach

RWA tokenization: The process of representing ownership or economic rights in a real-world asset as a cryptographic token on a blockchain, enabling fractional ownership, automated yield distribution, and programmable transfer compliance.

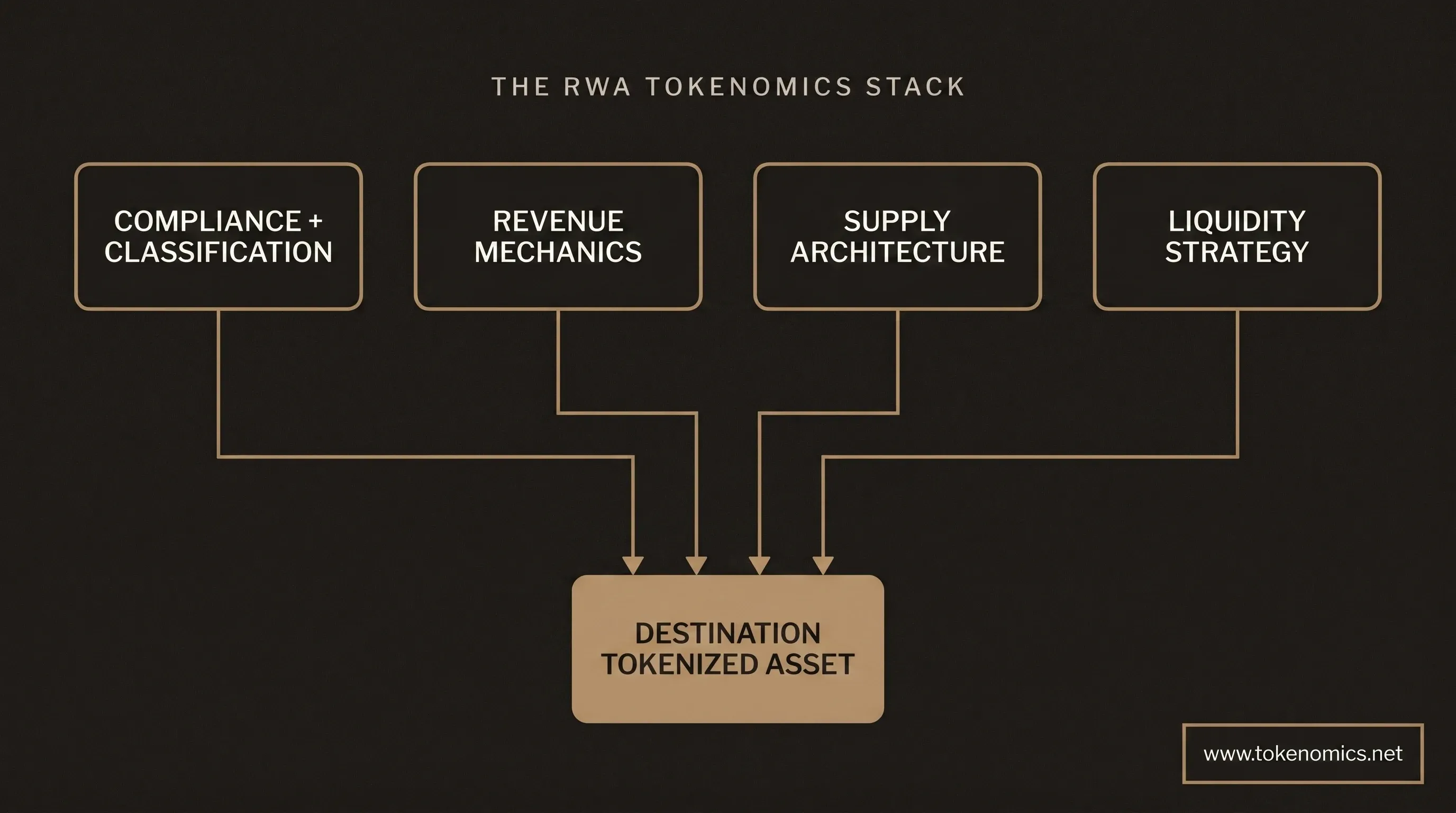

#The RWA Tokenomics Stack: Four Layers of Design

Every RWA tokenization follows the same design sequence regardless of asset class. We call this the RWA Tokenomics Stack. The four layers are not independent, each one constrains the layer below it. Designing them in parallel or out of sequence is the most common mistake we see across RWA engagements.

Layer 1: Compliance and Classification.

Before any mechanism design begins, answer three questions. First: is the token a security in the primary distribution jurisdiction? Second: what are the transfer restriction requirements for secondary market trading? Third: what on-chain identity verification infrastructure does your chosen token standard require?

These aren't design preferences. They're determined by the legal structure of the underlying asset, the distribution method, and the investor profile. The answers narrow your token standard options significantly.

ERC-3643 is the standard for tokenized securities requiring on-chain identity verification and transfer compliance enforcement at the smart contract level. It integrates ONCHAINID for investor identity, blocks transfers to unverified wallets automatically, and supports jurisdiction-by-jurisdiction compliance rules baked into the contract. ERC-1400 gives you partition management, the ability to split a token into tranches with different rights, but doesn't enforce identity verification natively. For many RWA tokenizations, especially regulated securities, the combination of ERC-1400 partition management with ERC-3643 compliance enforcement is the right architecture.

Get the legal opinion before choosing the standard. Always.

Layer 2: Revenue Mechanics.

How does value from the underlying asset reach token holders? Three patterns cover most RWA designs.

Direct yield distribution. Rental income, interest payments, or infrastructure fees paid on-chain to verified holders at set intervals. This is the most transparent structure: holders see the revenue, receive it in the denominated currency, and can calculate their yield. The tradeoff is operational complexity, you need reliable on-chain oracle infrastructure to bring off-chain revenue on-chain accurately.

NAV accrual. The token price appreciates as the underlying asset generates revenue; no interim cash flows are distributed. Holders realize value by selling the token at a higher price than they paid. This simplifies operations but creates investor relations challenges: holders can't observe yield, they can only observe price, and price is subject to secondary market conditions.

Hybrid. Partial distributions plus retained NAV growth. A private credit token might distribute 60% of interest payments while retaining 40% to grow the NAV. This is often the right structure for credit funds and infrastructure projects that need to reinvest a portion of returns.

A sustainable RWA revenue split across the portfolio typically looks like 60-70% to investors, 20-25% to protocol treasury, and 10-15% to operational reserve. The exact numbers depend on the asset class, the investor mandate, and the regulatory structure. Revenue comes first. Compliance comes second. Everything else follows.

Layer 3: Supply Architecture and Vesting.

Total supply, circulating supply, investor allocation, team allocation, treasury, and unlock schedules. For RWAs, vesting schedules are not just investor alignment tools, they are asset management tools.

High FDV / low float at launch creates sell pressure that erodes the distribution premium. If the token trades at a discount to the underlying asset's yield, the tokenization has failed. Design the circulating supply against the yield-expectation model, not against a speculation narrative.

Unlock events correlated with major asset valuation dates create predictable volatility. Property appraisals, credit rating reviews, and harvest cycles all produce moments when uncertainty is highest. Stagger unlock schedules away from those dates. This isn't just investor relations management, it's supply architecture. On-chain tokenized assets crossed $19B in 2025, up from $12B the year before (Source: RWA.xyz). That growth is pulling in institutional capital that reads your vesting schedule before they read your whitepaper.

Layer 4: Liquidity Strategy and Marketing.

A token without liquidity is a cap table, not a tradeable asset. Marketing is not adjacent to tokenomics design, it IS part of the design. KOL strategy, DEX listing depth, and market-making budget all affect whether the distribution premium holds.

For regulated RWAs, secondary market liquidity is often restricted to verified investors or specific exchange venues. ATS platforms in the US context, MTF venues in the EU context. This constraint shapes everything: the investor onboarding flow, the wallet infrastructure, the secondary market venue selection. Ignoring the liquidity constraint at design stage and planning to "figure it out after launch" is the most expensive design decision a founder can make.

Franklin Templeton's BENJI fund, BlackRock BUIDL, Ondo Finance, Maple Finance, and Centrifuge have all demonstrated that institutional capital will enter tokenized asset markets, but only when the liquidity infrastructure is present (Source: BlackRock 2025 Digital Assets Report). Designing tokenomics without a liquidity strategy is building for an audience that won't show up.

#Why RWA Tokenomics Is Different from DeFi Tokenomics

DeFi tokenomics starts with a token and works backward to find utility. Real world assets tokenization works the opposite way.

You start with an asset, a property, a credit facility, a solar farm generating cash flows, and you work forward to find the right on-chain representation. That reversal changes every design decision downstream. Tokenized real estate is the clearest example: the rental yield exists before the token does, and the tokenomics has to work around the property's lease structure, not the other way around.

In DeFi, the token IS the product. The emission rate, the staking yield, the governance weight, these are design variables you control from scratch. In RWA tokenization, the underlying asset is the product. It has a fixed contract, a fixed revenue schedule, and a fixed set of counterparties who don't care about your vesting schedule. Your tokenomics has to fit around something that already exists and has its own rules.

Three properties make this structurally different:

Revenue is external and constrained. A tokenized rental property pays rent on the property's lease terms, not on a schedule you set. If rent comes in monthly, your distribution mechanism has to reflect that. You can't emit your way out of a bad quarter.

Compliance determines which token standard is even possible before mechanism design begins. Most founders ask "what token standard should I use?" before they've answered "is this token a security in my primary distribution jurisdiction?" That's backwards. The legal classification narrows the technical options.

The investor base changes the liquidity equation. Regulated tokenized assets often target accredited or institutional investors with different liquidity expectations than a DeFi user farming yield at 200% APY. Designing for the wrong investor profile is a distribution problem waiting to happen.

ERC-3643: An Ethereum token standard for regulated securities that embeds on-chain identity verification and transfer compliance enforcement directly into the smart contract, using ONCHAINID for wallet-level accreditation checks. (Source: ERC3643 Association)

ERC-1400: A modular Ethereum security token standard that enables partition management, allowing a single token to be split into tranches with different rights, restrictions, and transfer rules at the smart contract level. (Source: ERC-1400 Standard Specification, ethereum.org)

Howey test: The four-part legal analysis derived from SEC v. W.J. Howey Co. (1946) that determines whether an instrument qualifies as an "investment contract" (and thus a security) under US law: an investment of money, in a common enterprise, with an expectation of profits, from the efforts of others.

#Compliance as the Foundation, Not a Feature

You can't bolt compliance onto a token that's already trading. The architecture needs to support it from day one.

The post-Tornado Cash, post-Coinbase, post-FIT-21 environment has made this unavoidable. Tornado Cash sanctions demonstrated that code is subject to OFAC controls. The Coinbase SEC complaint (2023) established that secondary market token trading can constitute a securities violation even without an ICO. FIT-21 draws explicit lines between digital commodities and digital securities that affect how a token's utility and governance functions are designed.

These aren't abstract precedents. They're the operating context for every RWA tokenization happening right now.

Compliance is the architecture, not a feature.

Three compliance questions every RWA design must answer before mechanism work begins:

Is the token a security? In the US context, this is a Howey test analysis specific to the offering structure, the token's economic rights, and the method of distribution. Most tokenized real-world assets with yield distribution components function as securities. The analysis is fact-specific and jurisdiction-specific. "Our legal team is looking at it" is not an answer that satisfies institutional investors.

What are the transfer restriction requirements? Regulated securities can only be transferred to verified, eligible holders. ERC-3643's ONCHAINID infrastructure enforces this at the contract level, transfers to unverified wallets fail automatically. ERC-1400's transfer restriction module requires explicit configuration. In both cases, the infrastructure has to be in place before the token goes live.

What KYC/AML obligations apply at the secondary market level? This depends on the jurisdiction and the secondary market venue. A US-domiciled ATS has different obligations than an EU-regulated MTF. The token's smart contract infrastructure must be compatible with whatever secondary market venues the token will trade on. Selecting the wrong token standard creates a technical incompatibility problem that surfaces after launch.

We design to make compliance review smoother. Whether a specific design qualifies for any exemption is determined by the legal team and the relevant regulator, not by the tokenomics firm. Per the firm's standard: RWA tokenization in this category typically requires jurisdiction-by-jurisdiction analysis, and we design with that constraint in mind.

#Revenue Design for Tokenized Assets: Getting the Economics Right

The token is not the product. The underlying asset's cash flow is the product. Everything else is plumbing.

This sounds obvious. Most projects don't design like it is.

After advising on RWA tokenization engagements, the revenue design failure patterns are predictable. These are the three we see most often.

Yield inflation at launch. Paying out a higher distribution than the asset generates for 6-12 months to attract buyers, then cutting back. This creates a distribution-cliff event: token price drops when yield normalizes, early holders exit, and the token's reputation for reliable yield is destroyed before the project reaches scale. The pattern is borrowed from high-APY DeFi farming, where it works because there's no underlying asset to anchor the yield, and applied to RWAs where it doesn't work because the underlying asset has a real revenue ceiling.

Treasury confusion. Using "treasury allocation" as a catch-all that functions as insider float. A 25% "operational reserve" with no lock-up schedule is community dumping rebranded. Institutional investors identify this immediately. The firm will not design extraction mechanics disguised as treasury management.

Ignoring the liquidity cost. Pricing the token distribution assuming holders will hold until maturity. They won't. Market-making budget is a cost that belongs in the financial model on day one, not a separate line item managed by a marketing agency with no visibility into the tokenomics.

How Monte Carlo simulation changes this: by running 10,000 iterations of the distribution model against asset-yield variance scenarios, liquidity depth conditions, and unlock events, the firm stress-tests the model before the token goes live. Abdur Rehman's Monte Carlo and agent-based modeling work on the Terra Luna post-mortem, analyzing how the death spiral mechanism compounded under stress, is the same methodology applied to validation before launch. The quantitative validation layer is what separates this from guides that describe the pattern without proving the model holds.

#Common Mistakes in RWA Tokenomics and What They Cost

After working through RWA tokenization engagements, the failure patterns are consistent. These aren't edge cases.

Designing the token before the legal structure. The token's properties, transferability, yield mechanism, secondary market eligibility, are all downstream of legal classification. Projects that design the token first spend 40-60% of their development time unwinding technical decisions when the legal structure comes in. We've seen this create 3-month delays at the point of exchange listing when the smart contract architecture couldn't support the transfer restrictions the legal team required.

Treating compliance as a post-launch patch. On-chain compliance isn't a software update. ERC-3643's identity registry must be populated before token distribution. ERC-1400's transfer restriction controllers must be configured at genesis. A token that goes live without these in place can't retrofit them without a full migration, which means a new contract, a new token, and re-kycing your entire investor base.

Ignoring distribution timing. Asset revenue events have predictable schedules. Quarterly rental distributions, monthly credit interest payments, annual harvest cycles. Vesting and unlock schedules that coincide with those events create double sell-pressure windows: holders receiving distributions and unlocked tokens simultaneously in the same market window.

Underestimating the liquidity problem. Regulated tokenized assets have constrained secondary markets. Founders discover this after launch when their investor base is holding illiquid tokens with no venue to trade them and no market-making infrastructure to support price discovery. 53% of tokens launched since 2021 are no longer trading (Source: CryptoRank). The liquidity problem is not unique to RWAs, but the constraint structure for regulated assets makes it harder to solve after the fact.

Conflating marketing with noise. Distribution is a liquidity problem. KOL allocation and market-maker budget are part of the tokenomics model, not a separate category managed by a different team with no access to the financial model. Marketing is liquidity. The projects that get this right build the marketing engine alongside the token design, not after it.

#The RWA Tokenomics Design Process: How We Approach an Engagement

This is what the work actually looks like. Not a pitch, a description of the process so you can evaluate whether the approach fits what you're building.

Phase 1: Asset classification and compliance architecture (2-3 weeks). Define the legal structure, jurisdiction strategy, and token standard selection before any mechanism design begins. The output is a classification memo (not a legal opinion, that comes from your legal team), a token standard recommendation with rationale, and a transfer restriction infrastructure specification.

Phase 2: Revenue model design and Monte Carlo validation (2-3 weeks). Model the distribution mechanics, stress-test against asset-yield variance, and set the financial projections. The output is a detailed revenue model, 10,000-iteration Monte Carlo simulation results, and a supply-demand projection that your legal team and institutional investors can audit.

Phase 3: Supply architecture, vesting, and liquidity design (1-2 weeks). Circulating supply plan, allocation table, unlock schedules timed away from asset valuation events, and a market-making budget recommendation based on the secondary market venue analysis. The output is an allocation table, a vesting schedule, and a liquidity strategy summary.

Phase 4: Complete data room production (1 week). The full tokenomics data room: mechanism design rationale, financial models, compliance-ready documentation, and investor-facing materials that hold up when lawyers and institutional investors look under the hood. Institutional capital requires institutional-grade documentation.

Total: 4-6 weeks. Competitor DAO reviews and freelancers have no accountability or timeline.

EcoYield Solar (a Tokenomics.net engagement) walked through this exact process for a solar infrastructure tokenization. The compliance architecture review revealed a token standard mismatch in the original design, caught at Phase 1, not at listing. The Monte Carlo validation surfaced a distribution-cliff scenario in the original yield model that the team adjusted before launch.

View our blog for more tokenomics guides

#Why RWA Tokenization Is Growing and Why Tokenomics Matters More Than Ever

On-chain tokenized real-world assets crossed $19 billion in 2025, led by cash equivalents, treasuries, and money market instruments (Source: RWA.xyz). 76% of global institutional investors plan to expand digital asset exposure in 2026, with tokenized assets as the primary expansion category (Source: EY-Parthenon Global Institutional Digital Assets Survey 2025).

Franklin Templeton's BENJI fund, tokenized money market instruments on Stellar and Polygon, exceeded $400M in AUM within 12 months of launch. BlackRock BUIDL reached $500M in weeks. Ondo Finance, Maple Finance, and Centrifuge are routing institutional capital through tokenized credit structures at a pace that would have been implausible 36 months ago.

This is not a niche. This is where the capital is moving. Your RWA strategy has to account for this environment: the institutional buyers are real, the compliance bar is real, and the market is selecting for founders who can prove both.

The tokenomics design discipline for real world assets tokenization is still being built. Most of the frameworks that work for DeFi tokenomics don't transfer cleanly. The firms that establish authority in this category now, through rigorous, quantitative, compliance-aware design work, will own the advisory relationship when tokenized asset volume scales past $1 trillion.

A tokenized asset without real cash flow underneath it is not an RWA. It's a speculation vehicle wearing RWA clothing. Revenue comes first.

#What Strong RWA Tokenomics Makes Possible

Get the four layers right and a set of outcomes follows that tokenized assets without rigorous design don't achieve.

Institutional investors can read your model. When the distribution mechanics, supply architecture, and compliance structure are documented at the same standard institutional due diligence requires, the investor conversation changes. It moves from "explain your tokenomics to me" to "let us review the data room." That's the difference between a fundraising conversation and a due diligence process.

Exchange listing gets simpler. Regulated exchanges and ATS platforms have their own compliance requirements for tokenized securities. A token built on ERC-3643 with a properly configured identity registry is a different conversation than a token built on ERC-20 that needs a compliance retrofit. The upfront architecture work pays its own cost.

The secondary market develops. When the yield is real, the supply architecture is clean, and the liquidity infrastructure exists, secondary market activity builds on something durable. Token velocity stays low, holders hold because the yield exceeds the friction of exit, and the market develops a genuine price discovery process.

Your team has something to give investors, lawyers, and developers. The complete tokenomics data room, mechanism design rationale, Monte Carlo models, compliance artifacts, legal opinion coordination, and investor documentation, enables every stakeholder simultaneously. Legal gets the compliance architecture. Developers get the specification. Investors get the model. Marketing gets the positioning.

Get your house in order before you go to market. That's what the design process delivers.

#Frequently Asked Questions

What is RWA tokenization?

RWA tokenization is the process of representing ownership or economic rights in a real-world asset as a cryptographic token on a blockchain. The token holds the legal claim or economic entitlement to the underlying asset. Real estate, private credit, infrastructure, commodities, and revenue-generating businesses can all be tokenized. The blockchain handles settlement, yield distribution, and transfer restriction enforcement.

What is the difference between RWA tokenization and DeFi tokenomics?

DeFi tokenomics designs the token first and works backward to find utility. RWA tokenomics starts from the underlying asset's cash flow and revenue structure and works forward to design the token wrapper. RWA tokenomics is constrained by the asset's legal classification, revenue timing, and investor base characteristics. DeFi tokenomics has design freedom; RWA tokenomics has design constraints that must be honored.

What token standard is used for RWA tokenization?

The two primary token standards for tokenized real-world assets are ERC-3643 and ERC-1400. ERC-3643 enforces on-chain identity verification and transfer compliance using ONCHAINID, making it the standard for regulated securities. ERC-1400 provides partition management, splitting a token into tranches with different rights. Many RWA tokenizations use both in combination: ERC-1400 for partition structure and ERC-3643 for compliance enforcement. The choice depends on the legal classification and jurisdiction of the token offering.

How does yield distribution work for tokenized real-world assets?

Tokenized real-world assets distribute yield through three mechanisms. Direct yield distribution pays rental income, interest, or infrastructure fees on-chain to verified holders at scheduled intervals. NAV accrual lets the token price appreciate as the asset generates revenue, without cash distributions. Hybrid structures combine partial cash distributions with retained NAV growth. The distribution mechanism must match the underlying asset's revenue schedule and the token's compliance structure. It cannot be designed independently of the legal framework.

What are the main risks of RWA tokenization from a tokenomics perspective?

The primary tokenomics risks in RWA tokenization are: designing the token before resolving the legal structure (creating costly mid-build unwinding); treating compliance as a post-launch patch (ERC-3643 and ERC-1400 compliance infrastructure cannot be retrofitted without a full migration); ignoring liquidity constraints for regulated secondary markets; yield inflation at launch to attract buyers; and underestimating the market-making budget required to maintain a secondary market for a compliant, restricted-transfer token.

How long does it take to design tokenomics for a tokenized real-world asset?

A complete tokenomics engagement for a tokenized real-world asset typically takes 4-6 weeks. Phase 1 (asset classification and compliance architecture) takes 2-3 weeks. Phase 2 (revenue model design and Monte Carlo validation) takes 2-3 weeks. Phase 3 (supply architecture, vesting, and liquidity design) takes 1-2 weeks. Phase 4 (complete data room production) takes 1 week. Projects that try to compress this timeline create compliance and design vulnerabilities that surface at listing or fundraising.

What is the Howey test and why does it matter for RWA tokenization?

The Howey test is the four-part legal standard from SEC v. W.J. Howey Co. (1946) used to determine whether an instrument is a security under US law: an investment of money, in a common enterprise, with an expectation of profits, from the efforts of others. Most tokenized real-world assets with yield distribution components satisfy the Howey test and are therefore securities. The implication is that the token must be issued and traded under an applicable securities exemption (such as Reg D or Reg S), which directly shapes the token standard selection, transfer restrictions, and secondary market venue choices.

RWA tokenization is not a shortcut to institutional capital. It's a compliance-aware, revenue-first design discipline applied to assets with real cash flows. The projects that get funded are the ones that can prove the model holds under scrutiny, quantitatively, legally, and operationally.

If you're building onchain and need your RWA tokenization to hold up under institutional scrutiny, book a strategy call. We'll assess your project and tell you whether we're the right fit. Sometimes we're not. We'll tell you that too.